Kerry Express (Thailand) PCL

SET:KEX

Decide at what price you'd be comfortable buying and we'll help you stay ready.

|

K

|

Kerry Express (Thailand) PCL

SET:KEX

|

TH |

|

A

|

AutoStore Holdings Ltd

OSE:AUTO

|

NO |

|

Humacyte Inc

NASDAQ:HUMA

|

US |

|

L'Occitane International SA

F:COC

|

LU |

|

LHN Ltd

SGX:41O

|

SG |

|

Elevation Oncology Inc

NASDAQ:ELEV

|

US |

|

Hino Motors Ltd

F:HMO

|

JP |

|

G

|

Gap Inc

XMUN:GAP

|

US |

|

Itesoft SA

PAR:ITE

|

FR |

|

V

|

Vintcom Technology PCL

SET:VCOM

|

TH |

|

IRIS Business Services Ltd

NSE:IRIS

|

IN |

|

AngioDynamics Inc

NASDAQ:ANGO

|

US |

|

B

|

Bangkok Dusit Medical Services PCL

SET:BDMS

|

TH |

|

Agilent Technologies Inc

NYSE:A

|

US |

|

S

|

Scansource Inc

F:SC3

|

US |

|

A

|

Abacus Mining and Exploration Corp

OTC:ABCFF

|

CA |

|

N

|

NETGEAR Inc

XMUN:NGJ

|

US |

|

A

|

Aurora Design PCL

SET:AURA

|

TH |

|

S

|

SBFC Finance Ltd

NSE:SBFC

|

IN |

|

Coplus Inc

TWSE:2254

|

TW |

|

A

|

Amada Co Ltd

F:AA2

|

JP |

|

Telkom Indonesia (Persero) Tbk PT

F:PTI

|

ID |

|

Azelis Group NV

XBRU:AZE

|

BE |

|

F

|

Fincanna Capital Corp

CNSX:CALI.X

|

CA |

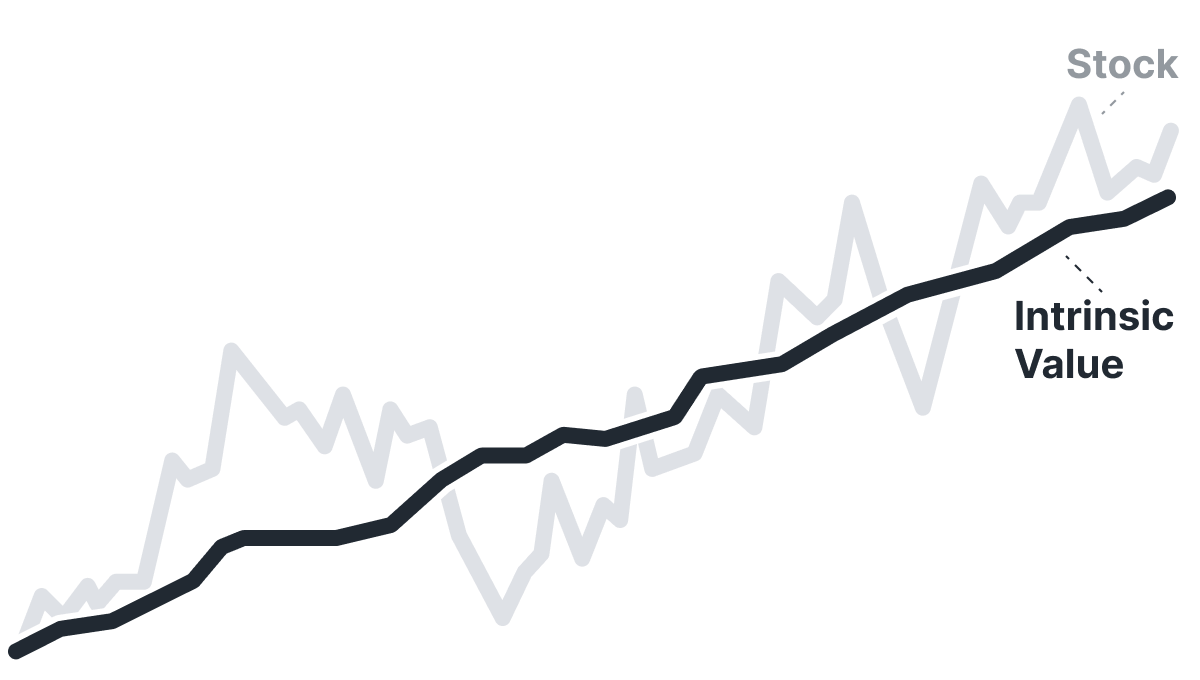

Intrinsic Value

The intrinsic value for Kerry Express (Thailand) PCL (KEX) under the Base Case is hidden THB. Compared with the current market price of 0.52 THB, the stock appears hidden .

KEX looks undervalued. But is it really? Some stocks live permanently below intrinsic value; one glance at Historical Valuation reveals if KEX is one of them.

Learn how current stock valuations stack up against historical averages to gauge true investment potential.

Let our AI compare Alpha Spread’s intrinsic value with external valuations from Simply Wall St, GuruFocus, ValueInvesting.io, Seeking Alpha, and others.

Let our AI break down the key assumptions behind the intrinsic value calculation for Kerry Express (Thailand) PCL.

The intrinsic value for Kerry Express (Thailand) PCL (KEX) under the Base Case is hidden THB.

Compared with the current market price of 0.52 THB, the stock appears hidden.