Delfi Ltd

SGX:P34

Decide at what price you'd be comfortable buying and we'll help you stay ready.

|

D

|

Delfi Ltd

SGX:P34

|

SG |

|

A

|

ABC Company SpA Societa Benefit

MIL:ABC

|

IT |

|

Breville Group Ltd

ASX:BRG

|

AU |

|

JCDecaux SE

PAR:DEC

|

FR |

|

Murray & Roberts Holdings Ltd

F:LDYA

|

ZA |

|

euromicron AG

F:EUCA

|

DE |

|

Ipsos SA

OTC:IPSOF

|

FR |

|

P

|

PRG Corporation PCL

SET:PRG

|

TH |

|

Sabina Gold & Silver Corp

TSX:SBB

|

CA |

|

Veeco Instruments Inc

NASDAQ:VECO

|

US |

|

Plazza AG

SIX:PLAN

|

CH |

|

Perficient Inc

NASDAQ:PRFT

|

US |

|

T

|

TROPHY GAMES Development A/S

CSE:TGAMES

|

DK |

|

E

|

Empresas Copec SA

SGO:COPEC

|

CL |

|

ARE Holdings Inc

F:A19

|

JP |

|

Applied Visual Sciences Inc

OTC:APVS

|

US |

|

D

|

Dito CME Holdings Corp

XPHS:DITO

|

PH |

|

F

|

Figene Capital SA

WSE:FIG

|

PL |

|

Badger Infrastructure Solutions Ltd

TSX:BDGI

|

CA |

|

R

|

Renasant Corp

F:RN6

|

US |

|

Galapagos NV

AEX:GLPG

|

BE |

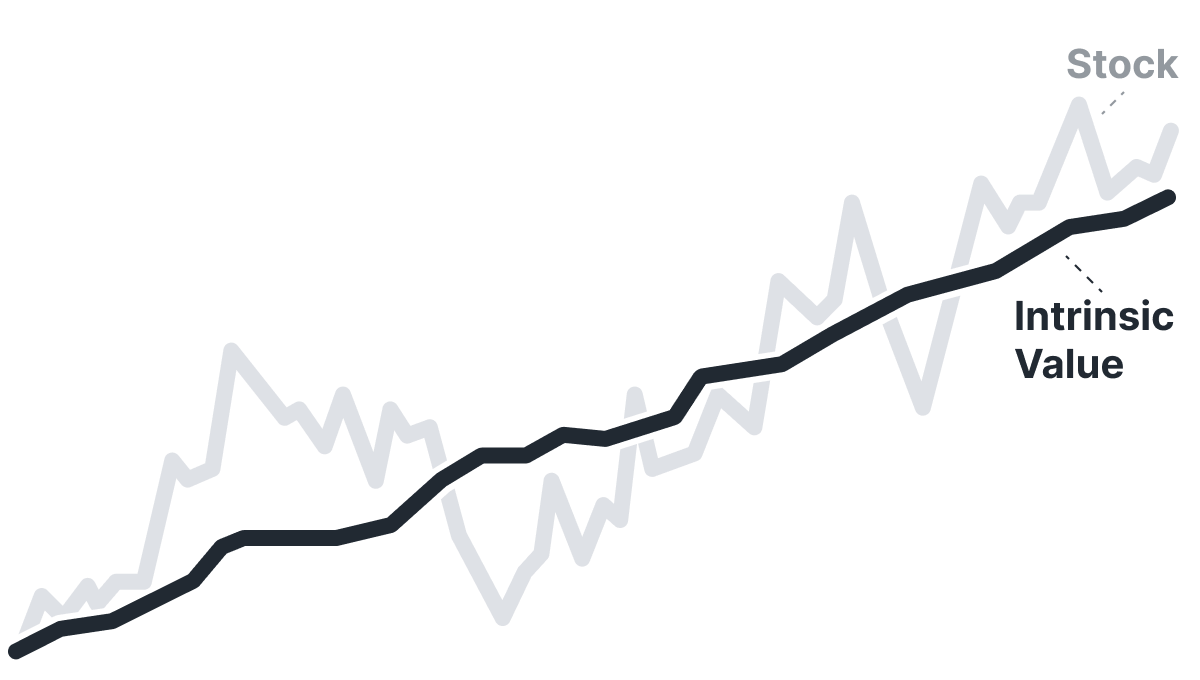

Intrinsic Value

The intrinsic value of one P34 stock under the Base Case scenario is hidden SGD. Compared to the current market price of 0.99 SGD, Delfi Ltd is hidden .

P34 looks undervalued. But is it really? Some stocks live permanently below intrinsic value; one glance at Historical Valuation reveals if P34 is one of them.

Learn how current stock valuations stack up against historical averages to gauge true investment potential.

Let our AI compare Alpha Spread’s intrinsic value with external valuations from Simply Wall St, GuruFocus, ValueInvesting.io, Seeking Alpha, and others.

Let our AI break down the key assumptions behind the intrinsic value calculation for Delfi Ltd.

The intrinsic value of one P34 stock under the Base Case scenario is hidden SGD.

Compared to the current market price of 0.99 SGD, Delfi Ltd is hidden .