Bodycote PLC

LSE:BOY

Intrinsic Value

The intrinsic value of one

BOY

stock under the Base Case scenario is

hidden

GBX.

Compared to the current market price of 734.5 GBX,

Bodycote PLC

is

hidden

.

BOY

stock under the Base Case scenario is

hidden

GBX.

Compared to the current market price of 734.5 GBX,

Bodycote PLC

is

hidden

.

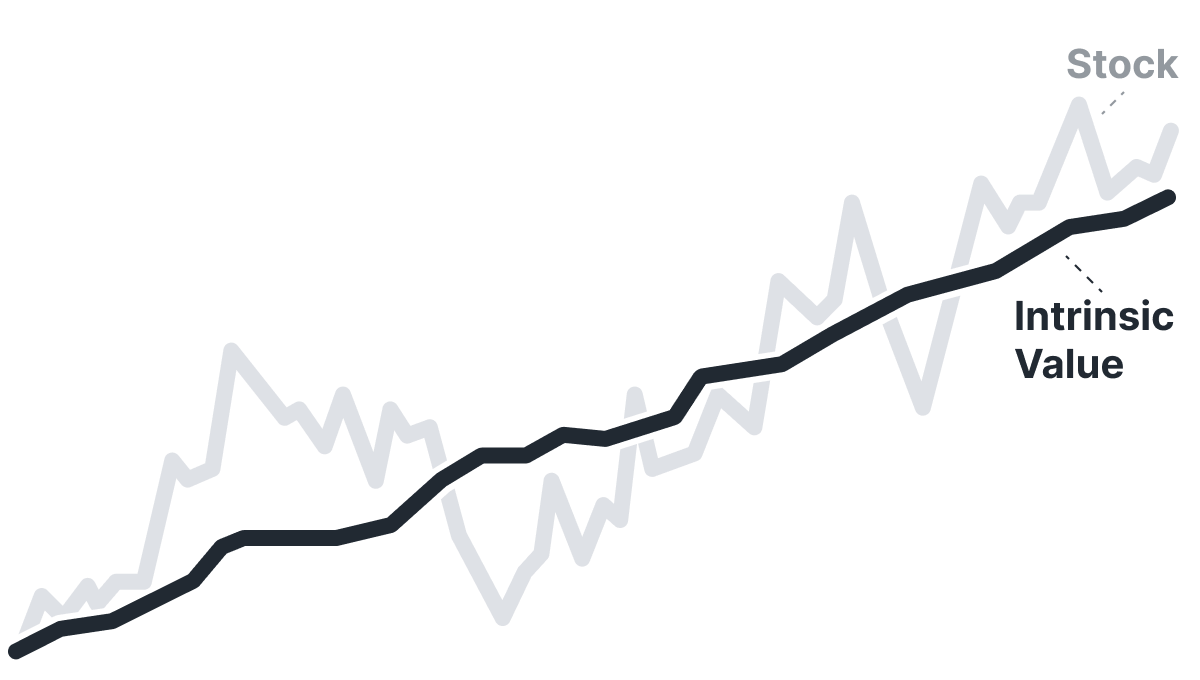

Valuation History

Bodycote PLC

BOY looks overvalued. Yet it might still be cheap by its own standards. Some stocks live permanently above intrinsic value; Historical Valuation reveals whether BOY usually does or if today's premium is unusual.

Learn how current stock valuations stack up against historical averages to gauge true investment potential.

Let our AI compare Alpha Spread’s intrinsic value with external valuations from Simply Wall St, GuruFocus, ValueInvesting.io, Seeking Alpha, and others.

Let our AI break down the key assumptions behind the intrinsic value calculation for Bodycote PLC.

The intrinsic value of one

BOY

stock under the Base Case scenario is

hidden

GBX.

Compared to the current market price of 734.5 GBX,

Bodycote PLC

is

hidden

.