eBay Inc

NASDAQ:EBAY

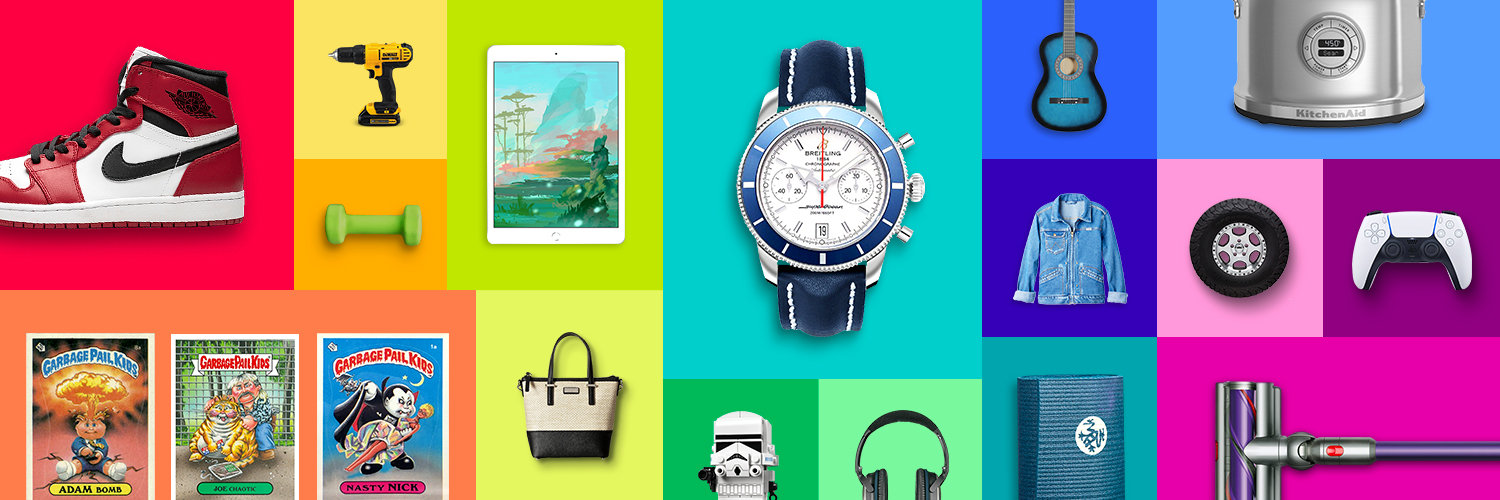

eBay Inc

In the bustling early days of the internet, amid a rapidly evolving digital landscape, eBay Inc. emerged as a pioneering force in online commerce. Born from a simple auction website founded by Pierre Omidyar in 1995, eBay transformed the way people bought and sold items. By connecting individuals and small sellers with potential buyers over the internet, eBay created a vibrant online marketplace that transcended geographic boundaries. Fast forward to today, and eBay operates as a global e-commerce behemoth, facilitating transactions through its platform where items can be bought and sold in a fixed-price format or through an auction model. This dual approach allows eBay to cater to a diverse range of sellers, from hobbyists and small businesses to larger enterprises, leveraging its vast marketplace to offer everything from vintage collectibles to brand-new consumer electronics.

At the heart of eBay's business model is the collection of fees related to this marketplace activity. It earns money primarily through listing fees, final value fees, and optional promotional services. Sellers are charged a percentage of the sale price when their items are purchased, and may also pay additional fees to increase the visibility of their listings. eBay has evolved beyond its original auction-based structure, integrating payment processing through its acquisition of PayPal (which has since been spun off) and, more recently, through its partnership with Adyen. This integration ensures a seamless transaction experience for users. Moreover, eBay invests significantly in technology and customer experience to maintain a safe and trusted platform, understanding that trust is essential for both its buyers and sellers. In leveraging a robust network and a trusted brand, eBay continues to thrive as a versatile player in the e-commerce arena, adapting to the changing needs and preferences of the digital shopper.

In the bustling early days of the internet, amid a rapidly evolving digital landscape, eBay Inc. emerged as a pioneering force in online commerce. Born from a simple auction website founded by Pierre Omidyar in 1995, eBay transformed the way people bought and sold items. By connecting individuals and small sellers with potential buyers over the internet, eBay created a vibrant online marketplace that transcended geographic boundaries. Fast forward to today, and eBay operates as a global e-commerce behemoth, facilitating transactions through its platform where items can be bought and sold in a fixed-price format or through an auction model. This dual approach allows eBay to cater to a diverse range of sellers, from hobbyists and small businesses to larger enterprises, leveraging its vast marketplace to offer everything from vintage collectibles to brand-new consumer electronics.

At the heart of eBay's business model is the collection of fees related to this marketplace activity. It earns money primarily through listing fees, final value fees, and optional promotional services. Sellers are charged a percentage of the sale price when their items are purchased, and may also pay additional fees to increase the visibility of their listings. eBay has evolved beyond its original auction-based structure, integrating payment processing through its acquisition of PayPal (which has since been spun off) and, more recently, through its partnership with Adyen. This integration ensures a seamless transaction experience for users. Moreover, eBay invests significantly in technology and customer experience to maintain a safe and trusted platform, understanding that trust is essential for both its buyers and sellers. In leveraging a robust network and a trusted brand, eBay continues to thrive as a versatile player in the e-commerce arena, adapting to the changing needs and preferences of the digital shopper.

Top Line Beat: eBay delivered better-than-expected Q3 results, with revenue up over 8% to $2.82 billion and GMV up 8% to $20.1 billion.

Profit Growth: Non-GAAP EPS rose over 14% year-over-year to $1.36, and non-GAAP operating income increased 9%.

Strategic Categories: Focus categories, especially collectibles and trading cards, grew over 15% and drove most of the overall growth.

Advertising Acceleration: First-party advertising revenue jumped nearly 23% year-over-year to $496 million.

AI & Innovation: Management highlighted substantial advances in AI-powered tools, magical listings, and agentic commerce platforms.

Guidance: Q4 revenue is expected between $2.83–2.89 billion and GMV between $20.5–20.9 billion, both growing year-over-year but at a slightly slower pace due to tougher comps and trade headwinds.

Investments: Continued strategic spending in eBay Live, shipping, vehicles, and AI, which is keeping margins flat to down near-term.

Shareholder Returns: Returned $760 million to shareholders in Q3, plans to return ~$3 billion in 2025.